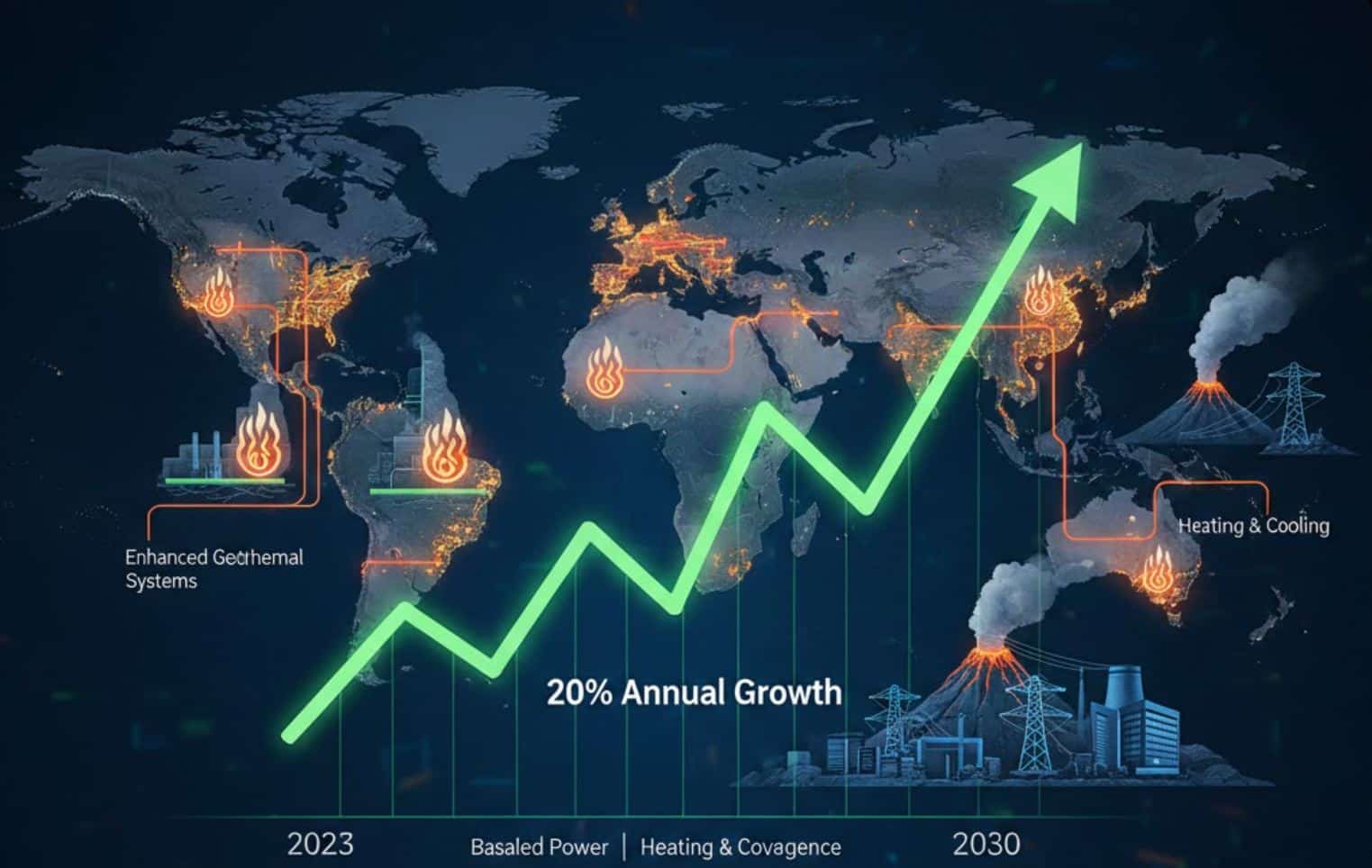

Global capital expenditure in geothermal energy is projected to increase approximately 20% annually through 2030, according to Rystad Energy analysis. This expansion marks a geographic shift beyond established markets in Southeast Asia and the United States, with Africa and Europe emerging as significant deployment regions driven by distinct demand profiles and technology applications.

The investment acceleration occurs amid widening recognition of geothermal’s baseload generation characteristics, though cost structures and capital allocation patterns reveal substantial variations between electricity-focused and heating-oriented projects. Regional divergence in technology priorities creates distinct market dynamics that will shape project economics and investor returns over the coming decade.

Capital Allocation Patterns and Pre-Development Risk

Rystad’s expenditure breakdown shows surface facilities consuming just over 50% of global geothermal capex, with subsurface drilling and completion work accounting for approximately 47%. Pre-final investment decision activities receive only 2% of capital despite representing the highest-risk phase, where exploration results determine project viability. This allocation pattern reflects the binary nature of geothermal development, where resource confirmation unlocks substantial follow-on investment but failed exploration yields limited salvage value.

The minimal pre-FID spending relative to total project costs creates a screening mechanism where only prospects with strong geological evidence or proven reservoir analogs attract exploration capital. This conservative approach may constrain the technology’s expansion into frontier geologies where resource potential remains unproven but could offer substantial reserves if successfully derisked through enhanced geothermal systems or other advanced techniques.

Regional Market Drivers and Technology Differentiation

United States geothermal activity centers on enhanced geothermal systems deployment and baseload power supply for data centers, a demand segment experiencing rapid growth as artificial intelligence workloads drive electricity consumption. EGS technology reduces geographic constraints by requiring only sufficiently hot rock rather than naturally occurring hydrothermal reservoirs, expanding the addressable resource base beyond conventional geothermal zones in the western states.

European markets prioritize district heating network decarbonization over electricity generation, reflecting the continent’s climate policy framework and existing thermal infrastructure. This application focuses on producing different cost structures and capacity factors compared to power generation projects, with district heating systems requiring approximately $3 per watt in capital expenditure versus $6 per watt for geothermal power plants, according to Rystad’s analysis.

Southeast Asian development, particularly in Indonesia, targets electricity generation to meet expanding grid demand in economies experiencing rapid industrialization and population growth. Indonesia’s position along the Pacific Ring of Fire provides access to high-grade geothermal resources suitable for cost-effective power generation, though transmission infrastructure and regulatory frameworks affect project economics and development timelines.

Cost Structure Analysis and Investment Implications

The $6 per watt capital intensity for geothermal power projects reflects expensive turbine equipment and surface infrastructure required for steam separation, condensation, and electricity generation. Binary cycle plants using organic Rankine cycle technology can reduce costs in moderate-temperature reservoirs but sacrifice efficiency relative to flash steam systems optimal for high-temperature resources.

District heating’s $3 per watt cost advantage stems from eliminating power generation equipment and directly utilizing geothermal fluid for thermal applications. This 50% capital cost reduction improves project economics in markets with heating demand and suitable distribution infrastructure, though it constrains applications to population centers with sufficient thermal load density to justify network investments.

These cost differentials influence regional investment patterns and technology selection. Europe’s heating focus aligns with lower capital requirements and existing district infrastructure, while Asia and North America’s electricity emphasis necessitates higher upfront costs offset by power purchase agreements and capacity market revenues. Investors evaluating geothermal opportunities must assess whether project returns adequately compensate for the technology path’s specific risk and cost profile.

Enhanced Geothermal Systems and Geographic Expansion

EGS technology’s advance reduces site-specific geological requirements by creating artificial reservoirs through hydraulic stimulation in hot rock formations lacking natural permeability. This approach borrows techniques from unconventional oil and gas development but applies them to heat extraction rather than hydrocarbon production. The expanded geographic applicability could accelerate deployment in regions without conventional hydrothermal resources, though EGS projects face higher drilling costs and reservoir sustainability questions compared to natural systems.

Commercial-scale EGS demonstrations remain limited globally, with most projects at pilot or early development stages. The technology’s economic viability at scale requires validation through sustained production across diverse geological settings. Rystad’s projection of EGS-driven growth in the United States assumes successful commercialization and cost reduction trajectories that have not yet materialized across a representative project portfolio.

Cooling Applications and Middle East Developments

Geothermal cooling represents an emerging application with particular relevance in Middle Eastern climates where air conditioning dominates electricity consumption. The UAE’s G2COOL project tests geothermal’s viability for space cooling through absorption chillers or direct use of cooler subsurface temperatures, potentially reducing fossil fuel consumption in cooling-intensive built environments.

Cooling applications face distinct technical and economic considerations compared to heating or power generation. Coefficient of performance metrics, distribution system requirements, and integration with existing building infrastructure affect project feasibility. The pilot project status indicates cooling remains in early commercialization phases, requiring demonstration before attracting substantial capital deployment.

Investment Prioritization and Resource Optimization

Rystad emphasizes cost structure understanding as essential for investment prioritization and maximizing geothermal resource value. Projects compete for capital not only against other geothermal opportunities but against alternative renewable technologies with different risk-return profiles and development timelines. Solar and wind power’s continued cost declines and rapid deployment cycles create comparison points for geothermal’s baseload generation premium.

Geothermal’s capacity factor advantages relative to intermittent renewables provide value in grids with high renewable penetration requiring firm capacity, though battery storage and natural gas with carbon capture represent competing solutions to intermittency. Whether geothermal’s 20% annual investment growth reflects fundamental economics or policy-driven deployment incentives will influence long-term capital sustainability as subsidies phase down and projects must compete on unsubsidized returns.

Regional market maturation will test whether early-stage enthusiasm translates to sustained capital allocation as projects move through development cycles and operational performance data accumulates. The technology’s expansion into Africa and nascent cooling applications adds geographic and technical diversity to the investment landscape but also introduces execution risks in markets with less-developed regulatory frameworks and supply chains compared to established geothermal regions.